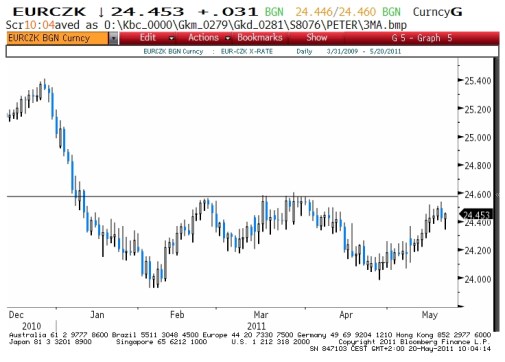

The Czech koruna strengthened slightly back to the 24.40 -24.50 EUR/CZK range and it seems that the pair currently does not feel like testing 200-day moving average (24.55). The koruna may have found some ground under its feet as US dollar weakness typically provides some relief. Nevertheless the Czech-euro negative interest rate differential is widening, which should continue to weigh on the Czech currency. The attractiveness of carry trades financed from the Czech koruna has risen given the widening negative interest rate differential, relatively low volatility of EUR/CZK and EUR/PLN and relatively low risk-free rates.

Speaking about rates – it’s quite remarkable that CZK FRA rates continue to fall despite weaker koruna and opposite development in the euro-zone. We believe that this trend will be reversed soon.

EUR/CZK. CZK used as funding currency for carry trades:

Forint finds ground after strong demand for bonds

The Hungarian forint appreciated about 1% D/D after the debt agency sold Ft95bn of bonds on Thursday and bids amounted to more than twice the offered amount. The pair climbed back into the 266-267 range, which was the trading range last week and thus it may target the key 265.00 level next.

The Polish zloty was oscillating around 3.92 EUR/PLN on Thursday.

Andrzej Bratkowski, a member of the Monetary Policy Council’s (MPC) hawkish camp, said yesterday that an acceleration of the hiking cycle was needed to prevent an increase in inflation expectations. Nevertheless, an unnamed source told Reuters today that nine out of ten MPC’s members voted for a rate hike in May. If this was true, then the situation in the MPC would be much less clear-cut than we had initially thought. Let us remind that the main argument for the hike was fear of inflation persisting above the inflation target in a medium term perspective due to the secondary effects of rising commodities prices.

It would be difficult to determine the mood of particular MPC members until the detailed information from April’s and May’s MPC meetings is known. As far as our expectations are concerned, we agree with the market and we expect two more rate increases this year, the first one in the Q3/2011 and the second one in Q4/2011.