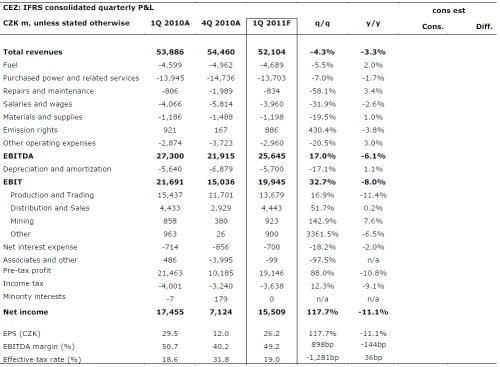

CEZ is scheduled to publish its 1Q11 results on 10 May 2011. We expect the firm’s EBITDA to come in at CZK 25.6bn (down 6% y/y) for 1Q11. Higher sales volumes will only partially offset lower electricity prices and less favourable FX hedging in the period. We forecast net profit at CZK 15.5bn (down 11% y/y) in 1Q11, a slightly bigger decline than EBITDA due to higher losses on the financial line related to carbon credit taxation. The reported result should be consistent with the company’s guidance for EBITDA at CZK 84.8bn in full-year 2011, thus we do not expect the earnings release to have any trading impact.

Production & Trading – We expect electricity production to increase to 19.2TWh in 1Q11, up both q/q (due to seasonally higher demand) and y/y. Nuclear-based generation should hold steady y/y with a brief maintenance shutdown at Dukovany (Unit 3) being counterbalanced by higher productivity. We forecast the average selling price to drop slightly to a baseload equivalent price of € 53/MWh in 1Q11, driven by lower hedging prices. Despite higher sales volumes, we project profit from the segment to come in at CZK 13.7bn in 1Q11, up 17% q/q but down year-on-year due to the increased use of less efficient coal-fired power plants and lower power prices.

Distribution & Sales – We expect seasonally higher demand and higher tariffs to push up segmental EBIT quarter-on-quarter in 1Q11. We forecast the division to generate an operating profit of CZK 4.4bn in 1Q11, up 52% q/q and broadly flat y/y.

Mining – We project the mining division to deliver an operating profit of CZK 923m (up 143% q/q and 8% y/y) in 1Q11. We estimate total coal sales at 5.4m tonnes (flat y/y) and the selling price to rise slightly (by 8% y/y) in 1Q11.

Financials (including associates and other) – We expect the firm’s net financial loss to more than double y/y in 1Q11. This should be due to additional charges for carbon credit taxation (estimated at CZK 0.7bn) being partly offset by an estimated CZK 0.3bn gain on the company’s (2 3805 HUF, -2,04%) option. All told, we forecast CEZ’s financials to record a net loss of CZK 0.8bn in 1Q11. We estimate the effective tax rate at 19.0% in 1Q11 versus 18.6% in 1Q10.