The worsening business sentiment across the developed world (Germany, United Kingdom, France, the United States) are increasing the likelihood of a recession within the next three to six months. Hence we have decided to explore how a moderate recession in the eurozone would impact on the Central European economies. Purely on the basis of our condensed historical experience, the Hungarian economy should be affected the most. Nevertheless in terms of its macroeconomic imbalances, the Hungarian economy is faring much better than before the crisis and, concurrently, a moderate recession in the eurozone (without any financial crisis) may have a shade different impact on all Central European economies than the recent devastating experience associated with the fall of the investment bank Lehman Brothers.

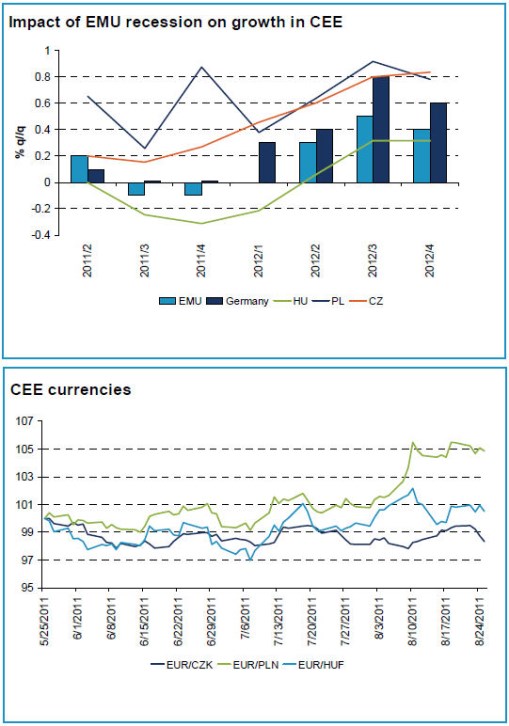

Our forecasts assume a moderate recession in the eurozone (-0.1% q/q for two consecutive quarters). We approximated the impacts on Central Europe with simple ARIMA models including few additional explanatory variables (GDP growth in the eurozone and Germany) estimated for the years 1995-2011, using quarter-on-quarter seasonally adjusted data. The figures, which are not at all surprising, indicate (see the graph below) that, on a cumulative basis, the moderate recession should have the greatest impact on the Hungarian economy and the least impact on the fairly closed Polish economy.

Nevertheless, our model forecast may be biased due to tough experience of the recent crisis, when the correlation of the individual economies with the rest of the world, particularly those that are very open, increased significantly. This may not necessarily reoccur if a milder crisis occurs. Therefore, if the eurozone goes through a conventional recession without a financial crisis, the negative impact on all economies may be smaller. For example, inventories may not be eliminated that dramatically (businesses no longer keep such large inventories) and layoffs will not be that huge (numerous businesses, notably in the Czech Republic and Hungary, already cut their HR costs to the bone during the recent crisis). Also, the availability of funds is unlikely to worsen to such a great extent, because the shock from foreign countries will mostly be purely real (a decline in contracts) rather than taking the form of financial contagion. In addition, Hungary, as a country, has become much less vulnerable to financial contagion, as its government has succeeded in turning significant current account deficits into surpluses.

In recent weeks/months, the Polish zloty (see the graph below) has been the Central European currency most affected by global risks. Nonetheless, given the significant likelihood of interventions by the Ministry of Finance (from abundant EU funding), the latitude for a further depreciation of this currency is limited. Both the Hungarian forint and the Czech koruna may still come under pressure and weaken, should the scenario of a ‘moderate recession’ in the eurozone happen. As we anticipate just a moderate recession in the eurozone, rather than hitting post Lehman-lows, the depreciation of all Central European currencies should be rather limited.